The Most Comprehensive and Up to Date 2024 Disability Tax Credit Guide. We Cover the Most Recent Info on the Application Process, Eligibility Criteria, T2201 Form, and How To Claim The Credit.

March 17, 2024 by dccinc

NOTE: This is the Ultimate 2024 Disability Tax Credit Handbook Guide, Your Go-To Resource for the Latest Regulations on Applying, Eligibility, Form T2201, and Claiming the Credit. Exciting news! Our 2024 Disability Tax Credit (DTC) guide has just been refreshed for March 2024. Stay informed with the latest updates from the Canada Revenue Agency (CRA) and gain valuable insights into maximizing your DTC benefits. Explore the newest changes and enhancements designed to streamline your application process and ensure you receive the support you deserve. Here are the key highlights to keep you ahead of the curve:

We hope that these updates will assist you in better understanding the DTC program and its eligibility requirements. Please note that if you have any questions or concerns, you can always consult one of our qualified professionals or contact the CRA directly for assistance.

Since its establishment in 1988, the Disability Tax Credit has served as a lifeline for countless Canadians grappling with disabilities. Despite its significance, many individuals and their healthcare providers still grapple with questions and barriers when it comes to fully harnessing its benefits. That’s where our comprehensive guide steps in. Crafted with care, it aims to demystify this invaluable government program and empower our community with knowledge. In 2024, amidst Canada’s economic landscape marked by nuanced challenges like a notable inflation slowdown and persistent COVID-19 pandemic repercussions, the importance of vital aids like the Disability Tax Credit remains unwavering. For individuals with disabilities, managing heightened healthcare costs, specialized services, and assistive devices can be a daunting task. Here, the DTC steps in, offering a financial lifeline by reducing income tax burdens and fostering economic resilience. Particularly in times of uncertainty, such support becomes paramount, providing a buffer for those facing employment barriers and financial instability. Thus, initiatives like the DTC play a pivotal role in alleviating economic strains for Canadians with disabilities.

Our goal is to make the DTC program more understandable and accessible to those interested in applying and to provide you with valuable information to help you build a strong case in your favour. We hope that by the end of this guide, you will have a better understanding of the DTC application and approval process, eligibility criteria, financial benefits, how to fill out Form T2201, and any additional resources that may support your case.

Once you are approved for the DTC, the government will reimburse you with retroactive tax credits for up to 10 years as well as an annual refund going forward. Moreover, you will gain access to a range of governmental and provincial benefit programs, including the Registered Disability Savings Plan (RDSP), to obtain additional financial assistance. Furthermore, it is worth noting that if you are applying for a child with a disability, you may qualify for an extra refund through the Child Disability Tax Benefit.

PLEASE NOTE: This guide has been written based on our extensive knowledge and years of industry experience to ensure its accuracy and comprehensiveness to educate and inform our fellow Canadians. However, this should not be used as a substitute for official documentation provided by the CRA on the DTC. Therefore, we request that you use it wisely!

Use Our Simple Calculator to Estimate Your Disability Tax Credits

Table of Contents

The Disability Tax Credit (DTC) is a non-refundable tax credit created by the Canadian Government and Canada Revenue Agency (CRA) and its purpose is to reduce the amount of income tax Canadians with disabilities and/or their families and supporters would have to pay annually hence assist with the various financial implications and expenses of having a disability or a substantial impairment. The DTC also provides an extra credit/refund (supplement) if the person found eligible is under 18 years of age at the end of the year.

The tax credit is broken down into Provincial and Federal amounts, with the Federal portion being the same across the country and the Provincial percentage varying from Province to Province.

To be found eligible for DTC, you must experience difficulty performing activities of daily living such as walking, feeding yourself, hearing, speaking, or other debilitating conditions that affect day-to-day living.

After you are found eligible for DTC, many other federal, provincial, or territorial programs such as RDSP , Canada Worker’s Benefit, and the Child Disability Benefit are available to you.

Use Our Simple Calculator to Estimate Your Disability Tax Credits

The Canada Revenue Agency (CRA) introduced the Disability Tax Credit program to help 27% of Canadians (CSD, 2023) and their families living with prolonged physical or mental impairments. The CRA created the program to offset the various costs associated with those impairments, such as medications, special equipment, personal support, etc. According to the findings from the most recent Canadian Survey on Disability (CSD), one in five Canadians (6.2 million) has one or more disabilities that restrict their daily activities performance.

Before 1986, the Canada Revenue Agency had a standard deduction reserved for individuals who used wheelchairs or were blind. When more disabilities and mental illnesses became more visible and recognized, the CRA introduced more taxable income benefits to those who suffered from these conditions.

In 2005, “prolonged impairments” became the definition to help people determine their eligibility. This definition created a path for persons with disabilities who struggled with everyday tasks to receive disability benefits.

Many individuals may not realize that receiving DTC approval can unlock various opportunities, enabling eligibility for additional federal, provincial, and territorial programs. These encompass essential initiatives like the Registered Disability Savings Plan (RDSP), Canada’s workers’ benefit, and the Child Disability Benefit, which are inaccessible without DTC qualification. DTC can provide crucial financial support, particularly for those facing financial hardships due to disabilities. For example, if you receive the Child Disability Benefit, that money can be utilized for professional help, accessible gadgets, and other necessities. Moreover, the DTC is structured to alleviate the burden of income tax payments, potentially resulting in savings on your forthcoming tax filings. In essence, the DTC is tailored to enhance your financial situation, making it imperative to explore application avenues if you meet the eligibility criteria.

There are two different levels considered when qualifying for the DTC: the first is disabled, meaning that you cannot perform basic activities in your daily life , and the second is slowed, meaning you take a significant amount of time to perform basic activities in your everyday life. Both disabled and slowed individuals can qualify for DTC, and both will receive the same level of benefits.

Many who consider themselves “slowed” never look into the DTC due to the perception that the benefit is only for those who are severely disabled. However, this is a misconception. Those who are slowed due to their impairments can also apply for DTC. For example, conditions like arthritis may cause a person to perform day-to-day tasks slower than others, making them eligible for DTC.

While the DTC provides more significant tax equity as well as assistance with disability costs that one may face, it does not in any way formally designate or label a person as disabled. The DTC was created to help impaired people who can still work and those who are too disabled to continue to work.

The DTC is a Federal tax credit program available to all Canadians and is administered by the Canada Revenue Agency (CRA).

The amount you receive from the government as a DTC consists of a Provincial amount and a Federal amount. The amount received is determined by the base Federal amount, which will be the same regardless of the province you live in, and the Provincial amount, which differs from Province to Province.

The DTC program was created to reduce the amount of income tax Canadians with disabilities must pay. Because of this, the Provincial amount changes based on the Province you live in, just as the amount of taxes you pay is different in each Province.

NOTE: In the “How Is the Disability Tax Credit Calculated?” we will touch more on how the amount you receive from Provincial and Federal sources is determined.

The DTC is a federal program and does not affect or alter your status of other government or provincial programs such as OSAP/student loans, ODSP (Ontario), AISH (Alberta), Disability Assistance (British Columbia), etc.

Once found eligible for the DTC, and as long as you are under 59 (must be under 49 to receive Government matching contributions) you are also automatically qualified to set up a Registered Disability Savings Plan (RDSP). The RDSP is a long-term savings plan providing benefits in disability savings, grants, and bonds.

As part of the DTC, the Child Disability Benefit is a tax-free monthly payment (not based on Federal taxes paid) made to families who care for a child under age 18 with a severe and prolonged impairment in physical or mental functions.

FIND OUT IF YOU ARE ELIGIBLE TO RECEIVE THE DISABILITY TAX CREDIT! Get a free assessmentThe following eligible disability categories, according to the Canada Revenue Agency (CRA), are as follows:

PLEASE NOTE: Eligibility for the DTC does NOT guarantee any benefits in the form of retroactive tax credits or refunds from the CRA. This is ONLY an indication that the CRA has judged your impairment as eligible for the DTC. It is important to note that if you or your supporter did not pay any taxes to the government during the eligibility period, you will not receive any money.

The Disability Tax Credit (DTC) program is intended to help Canadians who have prolonged or permanent impairments or the cumulative effects of significant limitations. According to the Canada Revenue Agency (CRA), eligibility conditions for the DTC program in Canada largely depend on an individual’s ability to perform “Activities of Daily Living” (ADL), such as bathing, dressing, walking, carrying, lifting, and other personal care activities.

To qualify for the DTC in Canada, you must first understand that eligible impairments are typically classified into 3 MAIN categories. However, it is important to note that eligibility for the DTC is not based on the diagnosis of the impairment, but rather on its severity and how it affects an individual’s ability to perform ADLs, as previously mentioned.

NOTE: The CRA updated the eligibility requirements for the DTC on June 23, 2022, allowing more individuals to apply. With that in mind, the updates to DTC eligibility mainly relate to mental functions (mental illness and psychological impairments) essential for daily life, as well as provisions for life-sustaining therapy for individuals with Type 1 diabetes.

The significant eligibility changes include:

PLEASE NOTE: Individuals whose applications for mental functions (mental illness and psychological impairments) or life-sustaining therapy were rejected after January 1, 2021, are not required to submit new applications. If an application was filed between January 1, 2021, and June 23, 2022, it will be reassessed according to the new eligibility criteria for 2023.

Understanding Cumulative Effect Eligibility is important for applying for the Disability Tax Credit (DTC):

There are 3 MAIN impairment categories eligible for the Disability Tax Credit (DTC), each with its own set of conditions. These categories are as follows:

As previously mentioned, having a medical practitioner certify that you have an impairment that falls under one of the following impairment categories does not necessarily make you eligible for the DTC. Eligibility is based on the severity of the impairment and its impact on one’s ability to perform “Activities of Daily Living.”

NOTE: The following sections will discuss each impairment category and the common conditions that usually make someone eligible for the DTC in Canada. Furthermore, under the sections on mental functions (mental illness and psychological impairments) and life-sustaining therapy, we will provide a more detailed account of the changes to the DTC eligibility requirements made by the Canada Revenue Agency for 2024.

Physical impairment covers a wide range of debilitating conditions that prevent someone from naturally living their day-to-day life. A physical impairment diagnosis is not enough to make one eligible for DTC; instead, eligibility comes from the diagnosis’s effects. The diagnosis must affect psychological activities of daily life such as making decisions, making judgments , memory, concentration, etc. The CRA considers the following conditions as potentially eligible physical impairments for the Disability Tax Credit:

Mental illness can have a profound impact on an individual’s ability to carry out daily tasks, and in severe cases can even impair their ability to take care of themselves without professional assistance or intervention.

According to the Canada Revenue Agency (CRA), you may be eligible for the Disability Tax Credit (DTC) if your mental functioning is deemed to be severe and prolonged, resulting in a marked restriction. This means that it affects your ability to perform the necessary mental functions of everyday life, referred to as “Activities of Daily Living” (ADL).

To clarify the current eligibility criteria for the DTC, it is important to note that for tax years up to 2021, the CRA deemed memory, adaptive functioning, judgment, problem-solving, and goal setting as essential mental functions for everyday life. However, in 2022, the CRA revised its eligibility guidelines, expanding the definition to include individuals who experience difficulty performing the mental functions necessary for everyday life, such as:

Bearing this in mind, the CRA considers the following conditions to be potentially eligible mental impairments for the DTC:

Neurological impairments affect the brain and prevent it from accurately or consistently controlling the body in severe cases. Working with a neurological impairment can be incredibly difficult as it makes things such as holding objects or walking independently challenging. CRA considers the following conditions as potentially eligible neurological impairments for the Disability Tax Credit:

“ Markedly restricted ” is also identified as a qualifying criterion when:

“Greg M, was diagnosed in 2005 with Osteoarthritis, underwent knee surgery in the same year due to tears in both knees. It takes him 3 times longer than a normal person to walk or perform any other activities in daily living. Greg has to sit to put on garments and socks. His wife does most of the housework due to his severe condition. Greg’s impairment is considered “markedly restricted” and his application was approved by the CRA”

Life-sustaining therapy is another marker of Disability Tax Credit eligibility. One must spend an excess of 14 hours per week on the treatment required for survival, such as insulin therapy , chest physiotherapy (helps with breathing), and kidney dialysis (blood filter).

That said, life-sustaining therapy often requires a substantial amount of time and money from individuals and their families, who rely on the treatment to perform their “Activities of Daily Living” (ADL). Therefore, individuals whose lives depend on life-sustaining therapy may be eligible to receive a non-refundable tax credit through the DTC program to help offset the medical expenses and lost income associated with such therapy.

“Louis G, suffers from Type 2 Diabetes, is presently on injections 4 times/day. He has to take diabetes related tests daily, which takes up over 2 hours per day, and more than 14 hours a week. The daily injections and tests Louis has to take is considered life sustaining therapy”

NOTE: Effective June 2022, the Canada Revenue Agency (CRA) has reduced the required frequency of life-sustaining therapy from three to two times per week; however, the criteria for 14 hours of weekly life-sustaining therapy remain unchanged. Moreover, as of the June 2022 update, individuals diagnosed with type 1 diabetes are deemed to have met the criteria for the DTC.

With that in mind, the CRA states that to be eligible for life-sustaining therapy in 2024 , the following criteria must be met:

Please keep in mind that the 14 hours dedicated to therapy only include the time taken away from regular daily activities specifically to receive therapy. This also includes the time needed to set up a portable device. However, if you need to regularly adjust your medication dosage, the time you spend determining and administering it can count towards the 14-hour-per-week requirement for the DTC.

Additionally, if your therapy necessitates the daily consumption of a special food or formula to manage your body’s needs, the time spent determining the appropriate amount can count towards the 14-hour weekly requirement. Similarly, if a child is too young to do the therapy activities, the time that another person spends doing and supervising those activities can count towards the 14-hour-per-week requirement.

The CRA has identified “prolonged impairment” as the working condition to determine one’s eligibility for the DTC.

The following is what they look for when determining if an impairment is considered prolonged:

The following is a list of some of the more common conditions the CRA considers when marking one’s eligibility for the Disability Tax Credit:

Autoimmune Diseases: Rheumatoid arthritis , Diabetes Type 1

FIND OUT IF YOU ARE ELIGIBLE TO RECEIVE THE DISABILITY TAX CREDIT!

The DTC is a refund on federal taxes paid by Canadian individuals with disabilities OR their supporters. i.e. if the disabled person or their supporter has paid or is paying federal taxes (usually above 20-25k income), they then can claim and receive a tax credit if approved for the Disability Tax Credit.

A key to understanding how the DTC application process works is to understand the differences between the disabled and the claimant.

When a person is applying for the Disability Tax Credit (DTC), they can be both the disabled and the claimant , but there are many situations where the disabled and the claimant are not the same person, so we must understand the difference between both.

The Disabled is the individual who has impairments or conditions that qualify them for the DTC.

In many cases, the person’s impairments may have prevented them from working and paying federal taxes. They will qualify for the DTC based on their impairments and can “transfer” those credits to their supporter, who will then become the claimant.

To be considered as a claimant by the CRA, you must meet the following criteria:

To learn more, please review the CRA’s information about Line 31800 – Disability amount transferred from a dependant.

NOTE: You cannot claim the disability amount that was transferred from the dependent for a child that you did not pay child support for. However, if separated from your spouse or common-law partner for a portion of the year you are applying for, special rules may apply.

You can split any unused part of the disability amount with an additional supporting person. However, the amount claimed for the dependent can’t be more than the maximum amount allowed for that dependent.

The DTC application process is made to be relatively straightforward and accessible to all persons interested in applying. There are two ways to fill out Form T2201, Disability Tax Credit Certificate, to apply for the DTC; digital application, and manual completion of the PDF. Both of these need to be filled out, completed, and signed by the individual applying, and their medical practitioner, before being submitted to the CRA for further assessment.

Qualifying and getting approved for the DTC is not always a simple process . A large percentage of Canadians who apply each year have their applications denied by the CRA.

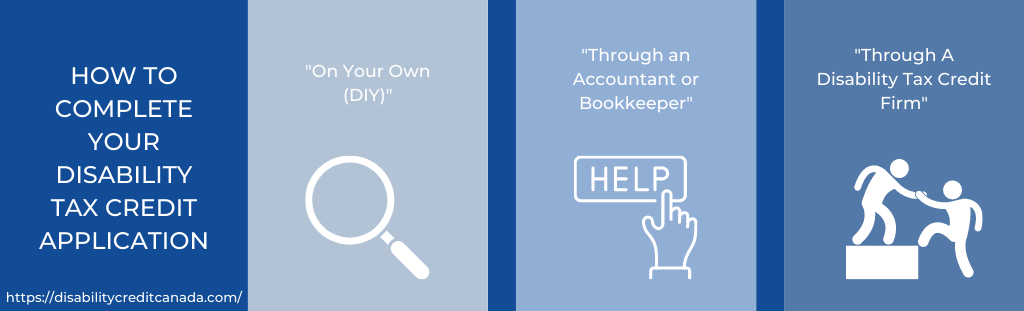

However, every person looking to apply is held to different circumstances. Therefore, we suggest that you consider one of the following routes for applying:

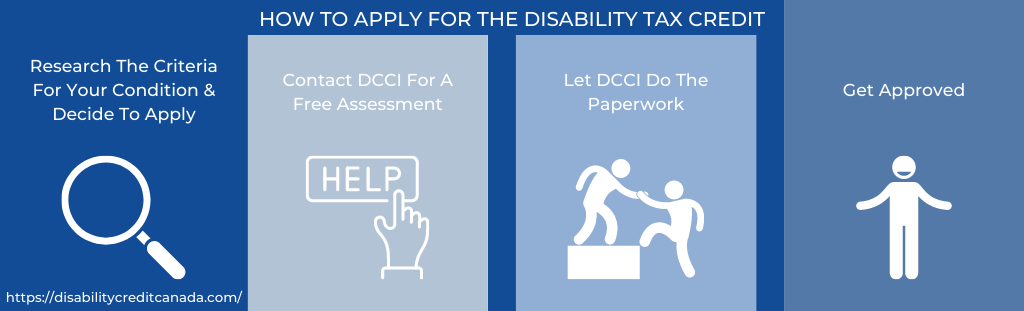

To apply for the Disability Tax Credit on your own, follow these steps:

The main benefit of taking this “DIY” route is the minimal cost associated with it. The only fee attached to applying independently is the one paid to the medical practitioner for filling out the form, which is usually a standard fee of $25 to $150.

As per Ontario Medical Association’s Physician’s Guide to Uninsured Services , This fee is capped at $44.95 for an authorized medical practitioner to fill out Part B of the form and certify your medical conditions, highlighted in Form T2201.

However, there are a few drawbacks to the “DIY” approach, such as:

NOTE: Although you are responsible for any fees that the medical practitioner charges you to fill out Form T2201. You may be able to claim those fees as a medical expense on line 33099 or 33199 of your tax returns.

Most accountants and bookkeepers look at the DTC as a part of the Canadian Tax code. Therefore, for them, your DTC application represents a simple tax document. Once you inform your accountant about your qualifying disability, they will print out the T2201 form and suggest that you have it filled out and commissioned by your medical practitioner.

Again, the main benefit of this approach is the minimal cost involved. Provided that most accountants/bookkeepers consider this a simple service and will not charge you for their advice.

However, there are a few drawbacks to using an accountant or bookkeeper to apply for the Disability Tax Credit, those are as follows:

The two options above can work well if the applicant’s impairments are severe, and their medical practitioner has experience and understanding of the eligibility criteria for applying for the Disability Tax Credit.

However, not all cases are as “clean-cut” and simple. Most DTC a pplicants fall into the “grey area” where the applicant may demonstrate some qualifying impairments but not enough to be found eligible according to the CRA guidelines.

NOTE: If your DTC application is denied by the CRA, reversing their decision can be a challenging process. You will have to “explain” your impairments in a different and more precise manner or possibly obtain the assistance of a new medical practitioner.

Some disabled Canadians choose to go with the third option of hiring a specialized Disability Tax Credit firm , to help them through the application process.

Although, there are many benefits to working with a specialized DTC firm (like Disability Credit Canada ), for instance:

The only drawback to working with a Disability Tax Credit Firm is the end fee if your application is approved. Once your application is approved and you receive the refunds you deserve, you are required to pay the DTC firm a certain percentage of the retroactive refunds reimbursed by them.

FIND OUT IF YOU ARE ELIGIBLE TO RECEIVE THE DISABILITY TAX CREDIT! Get a free assessmentRegardless of the method used to complete your Disability Tax Credit Application , it will typically take between 3 to 6 months for the CRA to assess the application and determine if you’re eligible for the Disability Tax Credit (DTC). However, this time frame can vary depending on the time of year, processing centre location, and the complexity of your impairment or application.

Furthermore, if your application is approved for previous years, your tax returns will have to be reassessed. As such, it may take 1-3 months or so to process your retroactive tax credits. On average, it will usually take 3 months to process a new application, but some can take up to a year before they are

NOTE: To quickly find out when you can expect the CRA to complete your request or get back to you about the status of your application, you can use the Check CRA Processing Times tool for further assistance.

There are several challenges involved with getting approved for the DTC. In this section, we will go over each in detail, and we’ll explain what you can do about it.

NOTE: In October of 2021 the CRA made substantial changes to the Disability Tax Credit Certificate to make it simpler and easier to complete.

The information below is a short explanation of the new Disability Tax Credit Certificate (T2201) and to learn more you can visit our t2201 Disability Tax Credit Certificate page .

Filling out Form T2201, Disability Tax Credit Certificate accurately is extremely important to the overall success and expediency of your Disability Tax Credit application. An y incorrect or insufficient information can easily lead to serious delays or even having your application denied.

Under the following section, we will be walking you through each part of Form T2201, Disability Tax Credit Certificat e, to make the application process easier to understand and complete.

To apply for the Disability Tax Credit (DTC) you must be a Canadian citizen or permanent resident and you must submit a certified Disability Tax Credit Certificate – T2201 to the CRA.

To complete Form T2201, first, you must fill out all personal details under the ‘individual’s section’ of the form, denoted Part A (pages 1-2).

Next, you must ask a medical practitioner to fill out and complete Part B (pages 3-16) of Form T2201. There they will answer a series of questions to provide detailed information on the impairments you or a family member are suffering from. Most importantly, your medical practitioner must explain in detail how the impairments you have affect your ability to perform “activities of daily living”.

NOTE: The Disability Tax Credit Certificate T2201 is available to download on the CRA’s website. Additionally, if your medical practitioner deems you eligible for the DTC, you can direct your medical practitioner to the digital application for medical practitioners .

Form T2201, Disability Tax Credit Certificate consists of 2 main parts:

Under the “Individual’s section,” of Form T2201, the CRA requires you to provide personal information for the disabled person and/or claimant. Some of the information you will be asked to provide is as follows: Name, Address, Date of Birth, and Social Insurance Number. Additionally, if you want to adjust your tax returns make sure that is indicated in question 3 of Part A .

Under the “Medical practitioner’s section” of Form T2201, your medical practitioner will be asked to fill out and certify the information provided in the sections that apply is correct and complete, then sign the form.

Life-Sustaining Therapy, Page 15: This page is only applicable to those persons who are using life-sustaining therapy.

FIND OUT IF YOU ARE ELIGIBLE TO RECEIVE THE DISABILITY TAX CREDIT! Get a free assessmentThis certification part of the form must be filled out by the correct medical practitioner (medical doctor, nurse practitioner, optometrist, speech-language pathologist, audiologist, occupational therapist, physiotherapist, or psychologist).

To be eligible to sign and certify Form T2201, Disability Tax Credit Certificate, the CRA will mandate that a “medical practitioner” must have been approved as a signing authority.